Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: preg_match() expects parameter 2 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 252

Warning: strlen() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 324

Mitsubishi Materials Issues ¥70 Billion in Euro-Yen Convertible Bonds; Share Price Falls

Mitsubishi Materials has issued two series of Euro-yen convertible bonds (CBs), each valued at ¥35 billion. In the stock market, the share price declined as investors reacted negatively to the potential increase in shares resulting from the issuance. The proceeds from this offering are earmarked for growth investments.

Mitsubishi Materials currently faces a situation w

here its cost of debt (approximately 5.5%) exceeds its return on assets (ROA) of 3.26%. In contrast, these CBs carry a 0% coupon rate, meaning no interest payments are incurred. Had the company raised the same ¥70 billion through a standard five-year domestic bond issue, the coupon rate would likely have been around 2.7% to 3.0%; thus, this CB issuance appears to be the right choice for the company.

here its cost of debt (approximately 5.5%) exceeds its return on assets (ROA) of 3.26%. In contrast, these CBs carry a 0% coupon rate, meaning no interest payments are incurred. Had the company raised the same ¥70 billion through a standard five-year domestic bond issue, the coupon rate would likely have been around 2.7% to 3.0%; thus, this CB issuance appears to be the right choice for the company.

However, the share price fell because the potential dilution—approximately 13.49 million shares—represents 10.26% of the total outstanding shares. This decline reflects the fact that conversion of the CBs would reduce earnings per share (EPS) by 10.26%.

When CBs are issued, hedge funds typically purchase them and then sell off only the straight bond component to buyers, effectively separating the CB into a bond and a warrant. Hedge funds seek the warrants to facilitate stock trading strategies based on “delta” (price sensitivity). Meanwhile, the straight bonds repurchased by securities firms are sold to end investors as “repackaged bonds.” Because these bonds are linked to the warrants, they are redeemed if the CBs are converted into stock. These repackaged bonds are structured to offer a higher yield than the company’s standard bonds of the same maturity, making them attractive to end investors seeking higher returns.

Let us examine the details of these CBs. A key feature of these two issues is the inclusion of conversion restriction clauses.

A conversion restriction clause stipulates that the bonds cannot be converted into stock unless specific conditions are met.・CB (Convertible Bond) due July 2030: Conversion into shares is permitted for the following quarter if the stock’s closing price exceeds 150% of the conversion price during the final 20 trading days of a quarter (up to the end of June 2029), or exceeds 130% thereafter. However, conversion is possible regardless of the stock price level from April 2030 until the conversion deadline of July 10, 2030.

Given the conversion price of 5,275 yen for the 2030 bonds, the 150% threshold corresponds to 7,912.5 yen, and the 130% threshold to 6,857.5 yen. In other words, conversion is not possible unless the stock price is at least 7,912.5 yen (until June 2029) or at least 6,967.5 yen (thereafter), with the exception of the period from April 2030 onwards.

・The terms for the 2032 bonds differ slightly in duration but are otherwise substantially similar, so details are omitted here.

The key factor for Mitsubishi Materials will be whether it can generate earnings and boost its stock price using the zero-cost funds raised.

Since the issuance of convertible bonds tends to create a “ceiling” on the stock price, the share price is likely to remain sluggish for some time.

・US: Key focus is on the CPI (14th) and PPI (15th)

Corporate earnings announcements in the US begin next week. Additionally, the CPI and PPI figures for June are due. Forecasts stand at 3.8% for CPI and 5.2% for core PPI. While the June figures are expected to fall below the May CPI level of 4.2%, they remain higher than the policy interest rate. Given current high stock price levels, a high reading could trigger a sharp decline; caution is advised.

Corporate earnings season also kicks off next week.

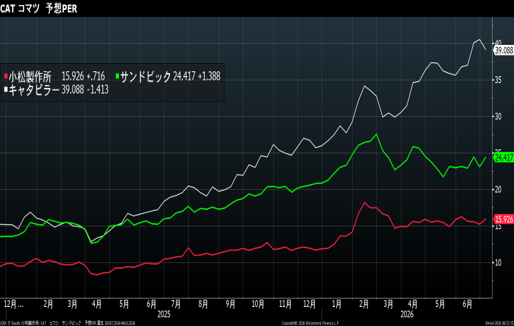

・Caterpillar-Komatsu Ratio: 11.90x

Caterpillar’s stock price is at a critical juncture. Its forward P/E ratio of 39x makes it more expensive than industry peers (Sandvik at 24x, Komatsu at 15.9x). The stock price has risen due to increased sales of generators for data centers. The question now is whether the AI-related bubble will burst; earnings results are due on August 4.

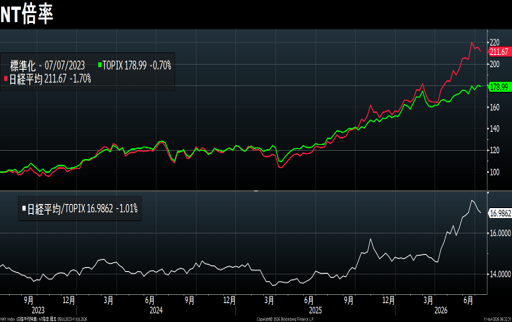

・Japan: NT Ratio Contracts to 16.98x

The NT ratio contracted as the Nikkei Stock Average fell 1.7% and the TOPIX fell 0.7% week-over-week.

The number of TOPIX-listed companies trading below a price-to-book (PBR) ratio of 1.0x stands at 568, a decrease of seven from the previous week.

Capital continues to concentrate in select semiconductor-related stocks.

However, with corporate earnings announcements approaching, significant upward momentum for semiconductor stocks is unlikely. The market is paying particular attention to Kioxia’s earnings, set for release on July 29, and whether the company can meet the exceptionally high expectations.

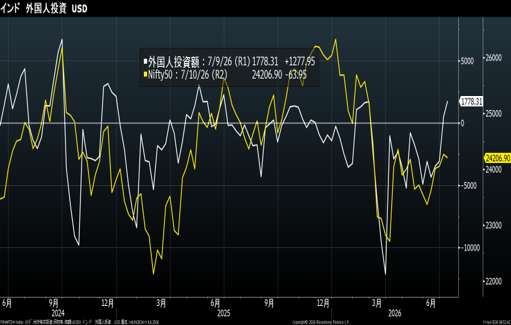

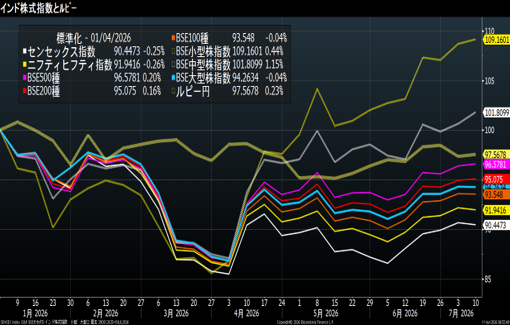

・India: Foreign Investors Net Buyers

While large-cap Indian stocks are struggling to break higher, the IPO market has seen stocks debut at prices 90% above their offering price. Teja Engineering Industries opened at 418 rupees—90% higher than its offering price of 220 rupees—and continued to climb, closing the week at a record high of 499.4 rupees.

Data: Bloomberg

Certified International Investment Analyst (CIIA)

Certified Securities Analysts Association (CMA)

AFP

Tadashi Fujii

投稿者プロフィール

-

大学時代から株式投資をはじめ、証券会社のトレーダーとなる。以後、30年

金融畑一筋。専門分野は債券、クレジット。

日本証券アナリスト協会検定会員(CMA)、国際公認投資アナリスト(CIIA)

詳しいリンク先はこちら