Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: preg_match() expects parameter 2 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 252

Warning: strlen() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 324

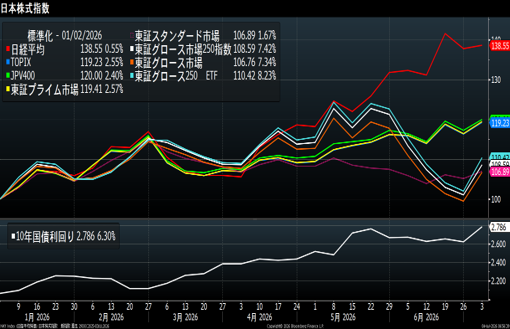

This week, the TOPIX rose by 2.55%, outperforming the Nikkei 225’s 0.55% gain, causing the NT ratio to drop to 17.15x. Capital flowed into value stocks for the first time in a while, reducing the number of stocks trading below a Price-to-Book Ratio (PBR) of 1.0x from 587 at the end of the previous week to 575. The issue of stocks trading below a PBR of 1.0x has been a major topic of discussion since March 2023, when the Tokyo Stock Exchange (TSE) announced measures urging companies to manage their businesses with a focus on the cost of capital and stock prices. Breaking down the PBR formula yields PBR = ROE × PER. While management cannot directly control the PER, they can influence ROE through actions such as share buybacks. Consequently, many companies have utilized surplus cash to repurchase their own shares. Additionally, an increasing number of companies are implementing measures to support their stock prices by raising dividend payouts.

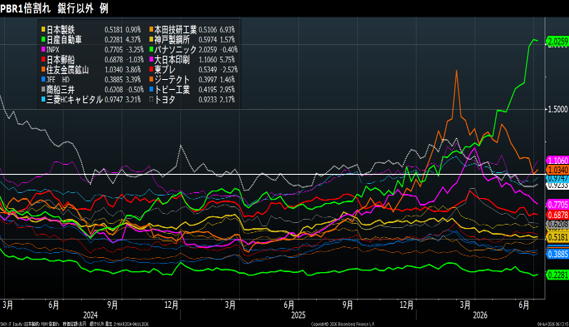

・Companies trading below 1.0x PBR: 10 in the S&P 500 vs. 575 in the TOPIX

Only 10 companies—approximately 2%—of the S&P 500 index constituents trade below a PBR of 1.0x, whereas about 35% of TOPIX constituents do so. The depreciation of the yen has further depressed Japanese stock prices; in other words, Japanese stocks appear cheap to foreign investors.

・After Real Estate, the Target is Stocks Trading Below 1.0x PBR

Prolonged deflation in the Japanese economy has widened the gap between domestic and global price levels. As a result, Japanese real estate prices appear undervalued to overseas speculators. The weak yen has

further amplified this sense of value, driving up real estate prices—particularly in Tokyo—fueled by speculative capital. Stocks trading below a PBR of 1.0x are likely the next target for these investors.・Examples of stocks trading below a PBR of 1.0x

Here are 10 examples of stocks trading below a Price-to-Book Ratio (PBR) of 1.0x, listed by descending order of market capitalization: Toyota (0.92x), Honda (0.92x), Japan Post (0.51x), Denso (0.66x), INPEX (0.77x), Central Japan Railway (0.66x), ENEOS Holdings (0.97x), Daiwa House (0.96x), Nippon Steel (0.52x), and Kansai Electric Power (0.73x). These are all blue-chip companies. However, there is a high probability that companies trading below a PBR of 1.0x will disappear from the market within the next decade.

・Japanese Government Bonds (JGBs): Sell-off in ultra-long-term bonds leads to yield curve steepening

In the JGB market, yields on ultra-long-term bonds (maturities exceeding 20 years) have risen, causing the yield curve to steepen. This movement reflects market caution regarding inflation. The depreciation of the yen is driving up import prices. The import price index is a leading indicator for the corporate goods price index, which in turn is a leading indicator for the consumer price index.

The Bank of Japan’s interest rate hikes have been insufficient so far; the policy rate will likely be raised to at least 1.5%.

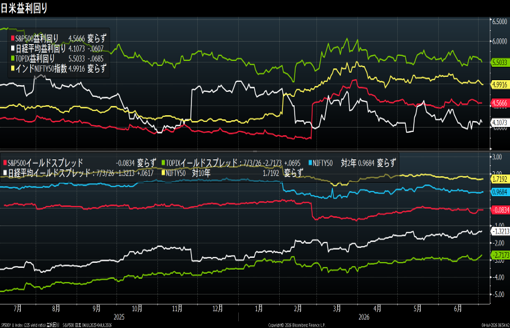

・Yield Spread: Negative in Japan

Although Japanese stocks are rising, the equity market remains undervalued compared to the bond market. A delay in the Bank of Japan’s policy adjustments is one contributing factor. With the TOPIX earnings yield at 5.5% and the JGB yield at 2.8%, the yield spread (JGB yield minus earnings yield) stands at -2.7%. In contrast, the spread for the S&P 500 is close to zero. This indicates that Japanese stocks are undervalued.

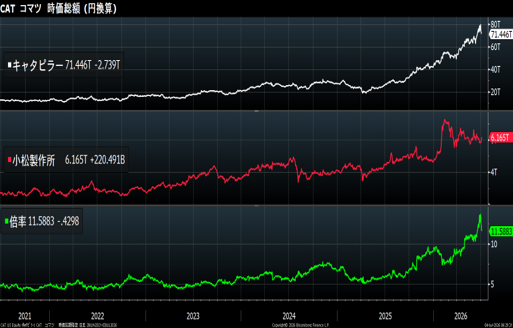

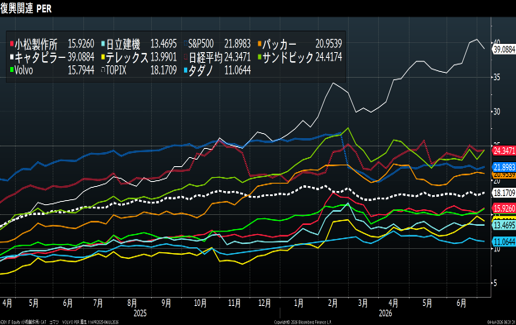

〇 Caterpillar-Komatsu Ratio

Caterpillar has a market capitalization of 71.44 trillion yen, while Komatsu’s is 6.165 trillion yen, resulting in a CAT/Komatsu ratio of 11.58x. Caterpillar shares have been sold off, while Komatsu shares have been bought. Caterpillar shares had been bought partly due to the AI boom, so the stock price falls when AI-related stocks are sold off in the US market. Caterpillar’s P/E ratio stands at 39x, which is high compared to Komatsu’s 16x and Sandvik’s 24x; AI-driven speculation may account for roughly 10 points of that multiple.

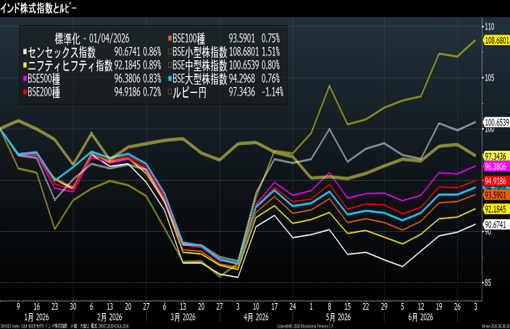

〇 India: Prime Minister Takaichi Visits India

Prime Minister Takaichi visited India and held talks with Prime Minister Modi, further strengthening the bonds between India and Japan.

The country has a median age of 28, and the “demographic bonus” period—defined as a state where the working-age population (15–64) is more than double the non-working-age population—is projected to last until around 2050. Japanese companies are increasingly expanding into the market and are well-positioned to contribute to India’s economic development.

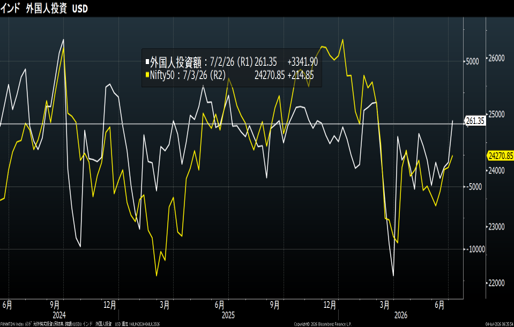

In the stock market, foreign investors have turned net buyers for the first time since February, with buying concentrated on small-cap stocks.

Data: Bloomberg

Certified International Investment Analyst (CIIA)

Certified Securities Analysts Association (CMA)

AFP

Tadashi Fujii

投稿者プロフィール

-

大学時代から株式投資をはじめ、証券会社のトレーダーとなる。以後、30年

金融畑一筋。専門分野は債券、クレジット。

日本証券アナリスト協会検定会員(CMA)、国際公認投資アナリスト(CIIA)

詳しいリンク先はこちら

未分類2026年7月4日日本市場はお宝でいっぱい、日本にはバリューがある

未分類2026年7月4日日本市場はお宝でいっぱい、日本にはバリューがある- 未分類2026年7月4日The Japanese Market is Full of Hidden Gems; Value Awaits

- 未分類2026年6月27日The Nikkei Average: A Plaything for Hedge Funds

- 未分類2026年6月27日日経平均はヘッジファンドのおもちゃ