Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: preg_match() expects parameter 2 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 252

Warning: strlen() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 324

Nippon Steel issued 600 billion yen in Euroyen bond certificates (CBs). The stock price fell 5.6% from the previous week due to concerns about dilution.

Two CBs were issued, one maturing in February 2029 and the other in February 2031, with an issue value of 300 billion yen each.

A notable feature of these CBs is their low conversion price (premium). The conversion price (exercise price) for the 2029 bond is 730.3 yen, a 10% premium over the benchmark stock price, and the 2031 bond is 737 yen, an 11.01% premium.

The premiums for the previous Euroyen CBs issued in 2021 were 31.99% for the October 2026 bond and 25.997% for the 2024 bond.

CBs are bonds that can be converted into stocks. They trade at a premium near their par value. The premium is the ratio between the CB’s theoretical price and its trading price. The December 2029 bond is currently priced at 105.609. The stock price at the end of the week was 636 yen, and the conversion price was 730.3 yen. The theoretical parity is 87.08, calculated by dividing the stock price by the conversion price. Since the market price is 105.609, the premium is (105.609 ÷ 87.08)

-1 = 21.26%. The premium is the option’s time value. This is because the conversion right for the CB expires on the maturity date. Therefore, when the remaining maturity is less than six months, even if the theoretical price is in the low 100s, the parity becomes negative and the bond will be converted into stock.

Furthermore, the parity decreases the further the stock price exceeds the conversion price. To give an idea, the parity becomes 0 at a theoretical price of 150, and above that, the parity becomes negative and conversion begins.

The setting of the CB conversion level this time is a burden on the stock price. This is because the closer the conversion price is to the stock price, the larger the delta (delta is the price sensitivity of a CB to a stock price).

It is important to understand the behavior of CBs and hedge funds. Generally, when Euroyen CBs are issued, hedge funds purchase them. They then sell the corporate bond portion of the CB to the buyer. In other words, the hedge fund’s position is limited to the CB’s conversion right (call option).

The corporate bonds repurchased by securities firms are repackaged as callable bonds and sold to end investors.

The hedge fund’s position in Nippon Steel is delta long. As the stock price rises, delta increases, and the delta-neutral position (the number of conversions multiplied by delta) grows, making the stock price more likely to fall. Hedge funds earn profits by selling shares.

The stock price is likely to remain sluggish for a while, but if some factor causes the stock price to surge and conversion proceeds, Nippon Steel’s equity capital will increase and its liabilities will decrease. In other words, it will have a positive financial effect. For Nippon Steel, converting its CBs is a mission. The question is, when and if the conversion will begin? You can check the status of CB conversion by checking the number of listed stocks at the end of the month on the Tokyo Stock Exchange.

CB conversion is likely to begin when the stock price is around 1,000 yen. The stock price will likely rise toward 1,000 yen.

– Japanese Stock Market: Value Stocks

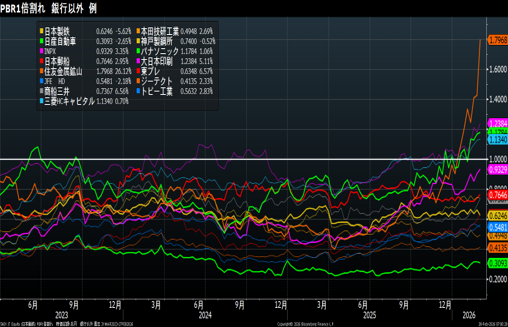

The number of stocks with a PBR below 1x is on the decline. As of February 26, 458 stocks in the TOPIX were trading below 1x. This is a decrease of 52 from 510 last week. Since there were 556 stocks at the end of January, approximately 100 stocks have a PBR above 1x in just one month. This trend is likely to continue.

![]()

It looks like there will be no stocks below 1x by the end of the year.

– Japanese Credit: Shrinking

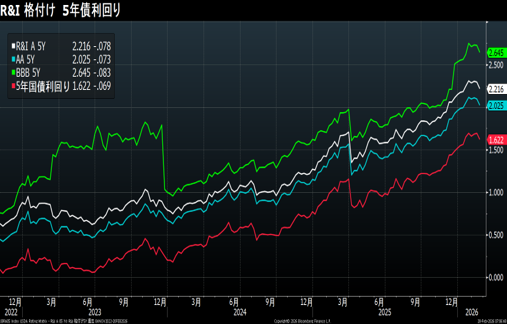

With two reflationary advocates appointed to the Bank of Japan’s board of directors, government bond yields have fallen. Corporate bonds are being bought, and total swaps are shrinking. Personally, I think a rate hike would be better.

Caterpillar vs. Komatsu Ratio: Shrinking to 7.69x

Caterpillar’s market capitalization is now ¥53.9 trillion, while Komatsu’s is ¥7 trillion.

US Stocks: Wait and See

US stocks are struggling to move higher. NVDA’s stock price is being pushed down by selling despite announcing strong earnings. It appears that the tech sector in general is experiencing a correction from its overbought status.

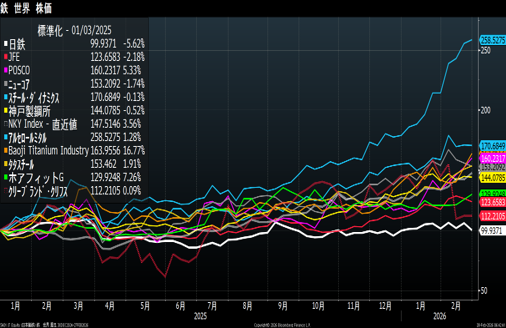

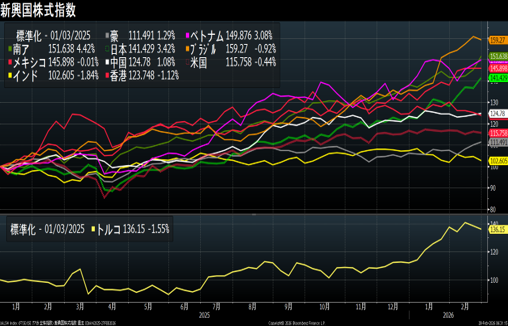

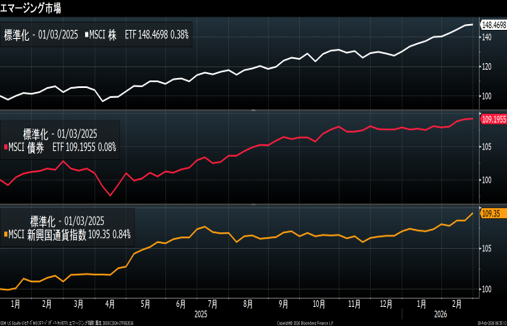

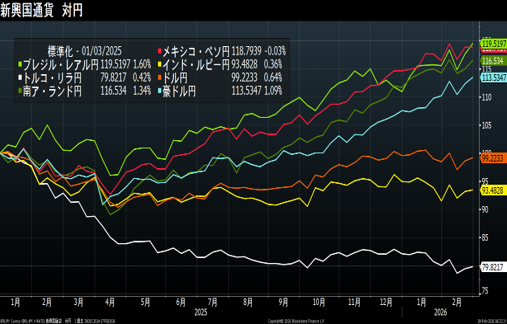

Funds are shifting from US stocks to Japan and emerging markets (Brazil, Mexico, and South Africa).

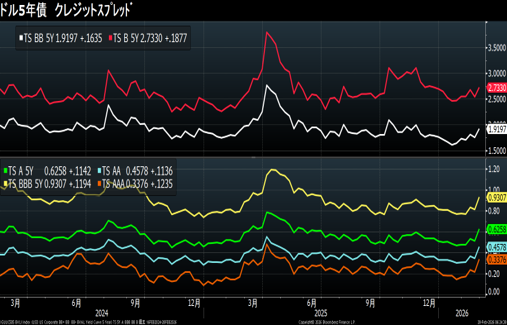

US Credit: Risk-Off

In the US bond market, funds are flowing from corporate bonds to government bonds.

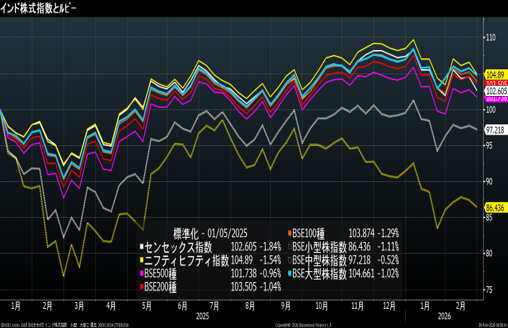

India: Fall

The Indian stock market is falling. Meanwhile, India’s GDP growth rate is steadily growing at 7.8% (expected 7.60%). Inflation is 2.75% (January). There are no inflation concerns and things are going well.

NISA savings accounts are a better option.

Data: Bloomberg

Certified International Investment Analyst (CIIA)

Certified Manager of Securities Analysts (CMA)

AFP

Tadashi Fujii

投稿者プロフィール

-

大学時代から株式投資をはじめ、証券会社のトレーダーとなる。以後、30年

金融畑一筋。専門分野は債券、クレジット。

日本証券アナリスト協会検定会員(CMA)、国際公認投資アナリスト(CIIA)

詳しいリンク先はこちら

未分類2026年7月25日Value Is the Way to Go

未分類2026年7月25日Value Is the Way to Go- 未分類2026年7月25日やっぱ、バリューだね

- 未分類2026年7月18日Is it the end of the world? Don’t worry! Japan has value stocks.

- 未分類2026年7月18日この世の終わりか?大丈夫!日本にはバリューがある