Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: strpos() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/compat.php on line 423

Warning: preg_match() expects parameter 2 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 252

Warning: strlen() expects parameter 1 to be string, array given in /home/tfujii46636/tadd3.com/public_html/wp-includes/class-wp-block-parser.php on line 324

Companies in Japan and the US are releasing their earnings reports one after another. The stock market is reacting with both joy and disappointment to these results. Some stocks are soaring, while others are plummeting.

Last week, Caterpillar, the largest construction equipment manufacturer in the US, and Komatsu, the second largest, released their earnings reports. Caterpillar’s results exceeded market expectations, causing its stock price to reach a new all-time high. Komatsu, on the other hand, suffered a sharp decline in its stock price due to poor performance. Although Komatsu announced a 100 billion yen share buyback, its stock price continued to fall.

As a result, Caterpillar’s market capitalization was 64.3 trillion yen, while Komatsu’s was 6.06 trillion yen, a ratio of 10.61 times (the largest ever).

What exactly accounts for this difference?

Stock Price

Caterpillar’s P/E ratio is 47x, its P/B ratio is 19.4x, and its dividend yield is 0.6%. Komatsu’s P/E ratio is 18.5x, its P/B ratio is 1.67x, and its dividend yield is 2.9%. Based solely on the indices, Komatsu appears undervalued.

Segments: Caterpillar is strategic, Komatsu is craftsman-based

Caterpillar’s segments are broadly divided into three areas: power and energy, construction, and resources. In the financial results announced for this fiscal year, sales totaled $17.415 billion (up 22.22% year-on-year), of which power and energy accounted for $7.031 billion (up 22% year-on-year), construction for $7.161 billion (up 38% year-on-year), and resources for $3.797 billion (up 4% year-on-year).

The increase in power and energy sales was due to increased sales of data center-related products and gas compression turbines. The increase in sales in the construction industry was driven by increased sales volume, price hikes, and increased sales to EAME (Engineering, Amusement, and Manufacturing).

Meanwhile, Komatsu’s segments consist of construction equipment and vehicles, retail finance, and industrial machinery, with construction equipment and vehicles accounting for approximately 92% of total sales.

For the fiscal year ending March 2026 (April 2025 to the end of March 2026), sales were 4.13 trillion yen (up 0.7% year-on-year).

Of this, construction equipment and vehicles accounted for 33.8 trillion yen (up 0.2% year-on-year), while sales from Sevmentol Station were sluggish at 491.1 million yen (down 18.0% year-on-year). By region, sales in Asia (excluding Japan and China) decreased by 32.9%, Oceania and Asia (excluding Japan) decreased by 14.2%, and Japan decreased by 4.6%. While sales in Europe, Central and South America, and Africa increased by more than 10%, this was not enough to offset the decline in sales in Asia.

Comparing them in this way reveals that these two companies have completely different business strategies. Caterpillar employs a strategic business development approach, while Komatsu relies on skilled craftsmen and a regionally dispersed business model.

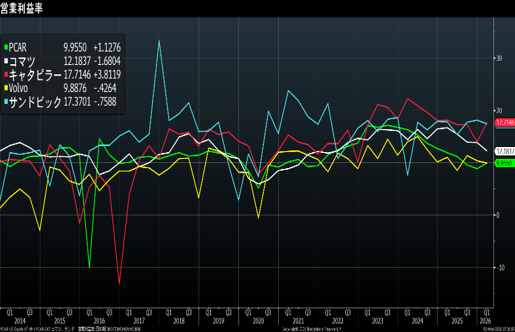

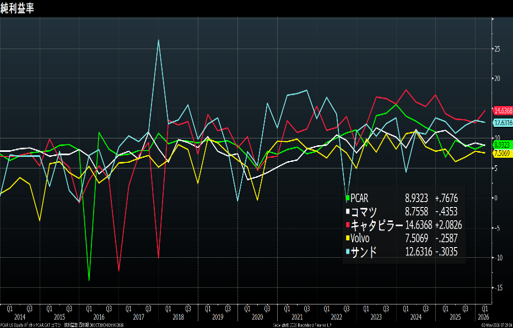

〇 Profit Margin

The operating profit margin (quarterly) was 17.7% for Caterpillar (up 3.8% year-on-year) and 12.18% for Komatsu (down 1.6%). The net profit margin (same period) was 14.6% for Caterpillar (up 2.0%) and 8.7% for Komatsu (down 0.4%).

〇 Outlook for the Next Period

Caterpillar is optimistic, backed by record-high order volume and revenue growth. On the other hand, Komatsu anticipates a decrease in revenue due to reduced demand in some regions affected by the situation in the Middle East and a decline in demand for mining machinery itself. Regarding profits, while efforts are being made to improve sales prices and reduce costs, a decrease in profits is expected due to rising costs, including the impact of US tariff policies, as well as increased fixed costs and decreased sales.

The stock price reacted straightforwardly. Will the gap in market capitalization continue to widen?

Komatsu’s strategy focuses on expanding into the Middle Eastern and American markets, including Saudi Arabia, Egypt, Jordan, and Pakistan, where market growth is expected to be high. Last year, they just signed contracts with the Pakistani government and provincial governments.

Komatsu has a strong, conservative approach, with a dividend payout ratio of over 40%, compared to Caterpillar’s 24.5%. Strategically, Komatsu is focused on self-preservation, while Caterpillar is more strategic.

From a stock investment perspective, if you prioritize dividends, choose Komatsu; if you prioritize growth, choose Caterpillar.

Data: Bloomberg

Certified International Investment Analyst (CIIA)

Certified Manager of Securities Analysts (CMA)

AFP

Tadashi Fujii

投稿者プロフィール

-

大学時代から株式投資をはじめ、証券会社のトレーダーとなる。以後、30年

金融畑一筋。専門分野は債券、クレジット。

日本証券アナリスト協会検定会員(CMA)、国際公認投資アナリスト(CIIA)

詳しいリンク先はこちら

未分類2026年8月1日Toyota’s PBR has risen above 1x—who’s next?

未分類2026年8月1日Toyota’s PBR has risen above 1x—who’s next?- 未分類2026年8月1日トヨタのPBRが1倍超え、次は誰だ!

- 未分類2026年7月25日Value Is the Way to Go

- 未分類2026年7月25日やっぱ、バリューだね